Double-entry bookkeeping produces reports that allow investors, banks, and potential buyers to get an accurate and full picture of the financial health of your business. You invested $15,000 of your personal money to start your catering business. When you deposit $15,000 into your checking account, your cash increases by $15,000, and your equity increases by $15,000. When you pay for the domain, your advertising expense increases by $20, and your cash decreases by $20.

Would you prefer to work with a financial professional remotely or in-person?

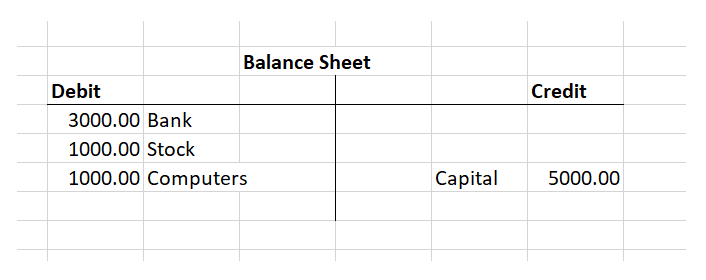

A better understanding of accounting principles is a must-have with this one, so this strategy may feel cumbersome if you’re a solopreneur or just starting out. Just as liabilities and stockholders’ equity are on the right side (or credit side) of the accounting equation, the liability and equity accounts in the general ledger have their balances on the right side. To increase the balance in a liability or stockholders’ equity account, you put more on the right side of the account. In accounting jargon, you credit the liability or the equity account. To decrease a liability or equity, you debit the account, that is, you enter the amount on the left side of the account. The first transaction that Joe will record for his company is his personal investment of $20,000 in exchange for 5,000 shares of Direct Delivery’s common stock.

Helps Companies Make Better Financial Decisions

The purpose of double-entry bookkeeping is to allow the detection of financial errors and fraud. An example of double-entry accounting would be if a business took out a $10,000 loan and the loan was recorded in both the debit account and the credit account. The cash (asset) account would be debited by $10,000 and the debt (liability) account is credited by $10,000. Under the double-entry system, both the debit and credit accounts will equal each other.

Brief History of Double-Entry Bookkeeping

Businesses should define these accounts beforehand — otherwise, you could end up with quite a complicated mess. This declaration is called a “chart of accounts.” Some examples might include cash, rent and supply accounts. Accountants usually first show the account and amount to be debited. On the next line, the account to be credited is indented and the amount appears further to the right than the debit amount shown in the line above.

Let’s define CRM

Additionally, the balance sheet, where assets minus liabilities equals equity, must also be balanced. The examples below will clarify the rules for double-entry bookkeeping. What causes confusion is the difference between the balance sheet equation and the fact that debits must equal credits. Keep in mind that every account, whether it’s an asset, liability, or equity, will have both debit and credit entries.

- This system is similar to tracking your expenses using pen and paper or Excel.

- At times this can involve reviewing dozens of journal entries, but it is imperative to maintain reliably error-free and credible company financial statements.

- Now, you can look back and see that the bank loan created $20,000 in liabilities.

- So, if assets increase, liabilities must also increase so that both sides of the equation balance.

- Double-entry bookkeeping shows all of the money coming in, money going out, and, most importantly, the sources of each transaction.

Keeping Accurate Books

Regardless of which accounts and how many are involved by a given transaction, the fundamental accounting equation of assets equal liabilities plus equity will hold. A general ledger represents the record-keeping system for a company’s financial data, with debit and credit account records validated by a trial balance. It provides a record of each financial transaction that takes place during the life of an operating company and holds account information that is needed to prepare the company’s financial statements. Transaction data is segregated, by type, into accounts for assets, liabilities, owners’ equity, revenues, and expenses.

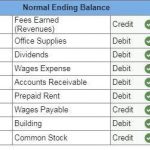

Assets, Expenses, and Drawings accounts (on the left side of the equation) have a normal balance of debit. Liability, Revenue, and Capital accounts (on the right side of the equation) have a normal balance of credit. On a general ledger, debits https://www.business-accounting.net/preferred-synonyms-antonyms/ are recorded on the left side and credits on the right side for each account. Since the accounts must always balance, for each transaction there will be a debit made to one or several accounts and a credit made to one or several accounts.

The debit entry increases the wood account and cash decreases with a credit so that the total change in assets equals zero. Liabilities remain unchanged at $0, and equity remains unchanged at $0. Credits increase revenue, liabilities and equity accounts, whereas debits increase asset and expense accounts. Debits are recorded on the left side of the general ledger and credits are recorded on the right.

You’ll be ahead of the game if you’re already using double-entry bookkeeping. Plus, more accurate data means they can give you better advice on tax deductions and the financial health of your business. Both Cash and Fixed Asset are asset accounts, so a credit represents a decrease in the account balance while a debit represents an increase. https://www.online-accounting.net/ Debits increase expenses and assets and decrease liability, revenue, or equity accounts. Credits increase liability, revenue, or equity and decrease asset and expense accounts. It involves making sure your debits and credits agree in a double-entry accounting system.If that all sounds like a foreign language, don’t give up just yet!

The early beginnings and development of accounting can be traced back to the ancient civilizations in Mesopotamia and is closely related to the development of writing, counting, and money. The concept of double-entry bookkeeping can date back to the Romans and early Medieval Middle Eastern civilizations, where simplified versions of the method can be found. Most modern accounting software, like QuickBooks Online, Xero and FreshBooks, is based on the double-entry accounting system. The accounting system might sound like double the work, but it paints a more complete picture of how money is moving through your business. And nowadays, accounting software manages a large portion of the process behind the scenes.

A debit is made in at least one account and a credit is made in at least one other account. For the accounts to remain in balance, a change in one account must be matched with a change in another account. Note dividends that the usage of these terms in accounting is not identical to their everyday usage. Whether one uses a debit or credit to increase or decrease an account depends on the normal balance of the account.

In accounting, a general ledger is used to record a company’s ongoing transactions. Within a general ledger, transactional data is organized into assets, liabilities, revenues, expenses, and owner’s equity. After each sub-ledger has been closed out, the accountant prepares the trial balance.